PUBLISHED ON:

December 09 2025

The Strangler-Fig Approach to Introducing Agentic AI in Insurance Platforms

A Controlled, Evolutionary Model for Modernizing Core Systems Without Disruption

A Controlled, Evolutionary Model for Modernizing Core Systems Without Disruption

Insurance core systems are under increasing pressure.

Most insurers recognize the need for modernization.

However, full core replacement programs are:

The strategic question is no longer:

“How do we replace the core?”

It is:

“How do we evolve the core safely while introducing intelligent automation?”

This white paper outlines how the Strangler-Fig architectural pattern can be applied to introduce Agentic AI into legacy insurance platforms — without a high-risk, big-bang transformation.

Traditional core insurance systems were built to:

They were not built to:

As a result, insurers face two flawed options:

Neither option provides a sustainable path forward.

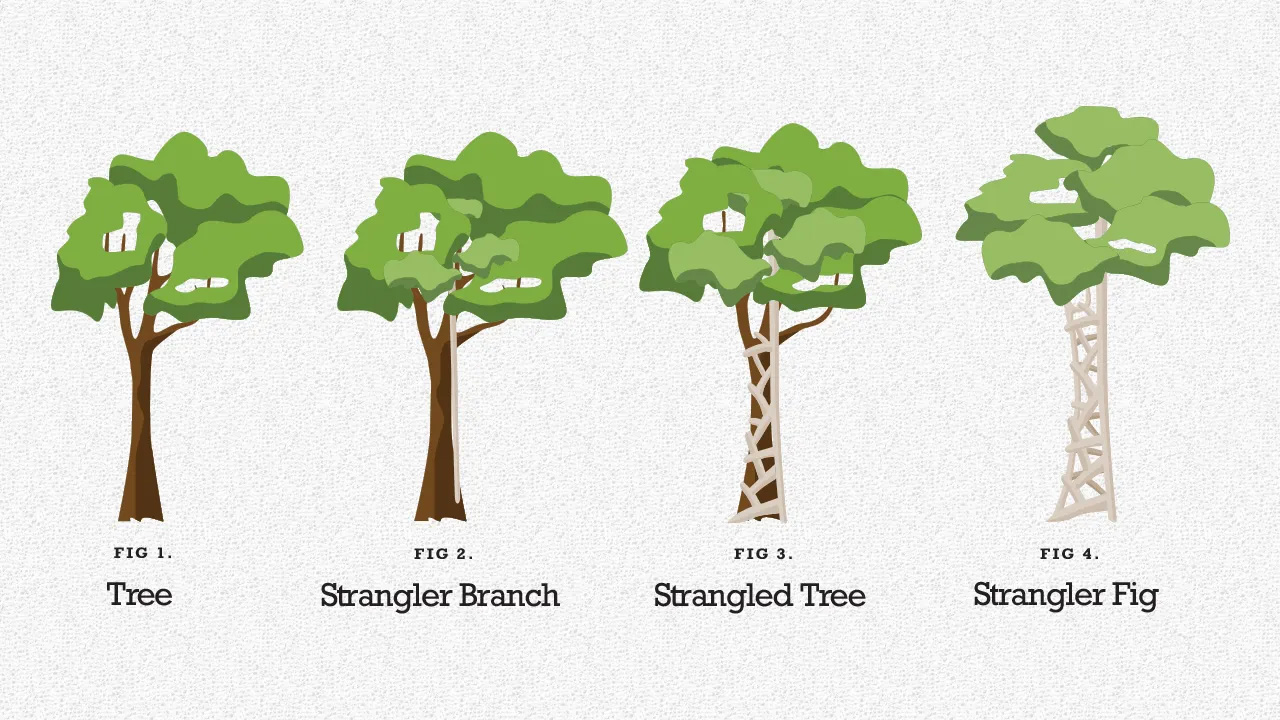

The Strangler-Fig pattern is a modernization strategy in which:

Rather than replacing the monolith in one event, modernization becomes evolutionary.

When applied to Agentic AI, this pattern allows insurers to introduce intelligent automation safely — without destabilizing existing underwriting and claims engines.

Introducing Agentic AI into insurance platforms requires architectural discipline.

The recommended approach involves five progressive layers:

Step 1: Wrap the Core With a Semantic Layer

Before introducing AI agents, insurers must:

This semantic layer becomes the grounding context for AI.

Without it, agents will amplify ambiguity.

Step 2: Introduce Transformation-Driven Gold Data Layers

Legacy insurance systems often store operational data in:

Using a medallion architecture (Bronze → Silver → Gold):

This step is foundational.

Agents must operate on transformed, validated data — not raw transactional tables.

Step 3: Extract Business Logic Into Middleware Services

In most legacy insurance platforms, business rules are:

These rules must be abstracted into:

This enables:

Over time, decision intelligence shifts from the database to modular services.

Step 4: Deploy Domain-Constrained AI Agents Outside the Core

Instead of embedding AI directly inside the core platform, deploy specialized agents around it.

Examples:

Claims Agent

Pricing Agent

Compliance Agent

These agents:

They augment the core — without destabilizing it.

Step 5: Gradually Shift Decision Intelligence Away From the Monolith

Over time:

The platform becomes:

This is modernization without disruption.

Agentic AI in insurance must operate within strict governance frameworks.

Key principles include:

Domain Confinement

Agents must operate only within their defined business domain.

Orchestration Layer

An AI orchestration layer routes tasks, enforces validation gates, and logs actions.

Phased Autonomy

Deployment should follow a staged approach:

Auditability

Every decision must be:

In regulated industries like insurance, autonomy without governance is unacceptable.

Applying the Strangler-Fig approach to Agentic AI enables:

Reduced Modernization Risk

No big-bang system replacement.

Faster Time to Value

Agents deliver operational improvements early.

Improved Compliance

Continuous monitoring and structured audit trails.

Operational Efficiency

Automation of low-value, repetitive workflows.

Long-Term Platform Flexibility

Gradual evolution into modular, AI-ready architecture.

The insurance industry is facing:

Full core replacements are often unrealistic.

But incremental intelligence adoption is achievable.

Agentic AI does not require destruction of legacy systems.

It requires architectural strategy.

The future of insurance modernization is not radical replacement. It is structured evolution.

The Strangler-Fig approach provides a disciplined path to:

Modernization does not require disruption.

It requires:

Governance first.

Semantics first.

Controlled autonomy.

In insurance, intelligence must scale — but it must scale safely.

ZeroToSixty, Inc.

2261 Market Street, STE 5959

San Francisco, CA 94114

United States

+1 (415) 818-0260